By: Nate Bek

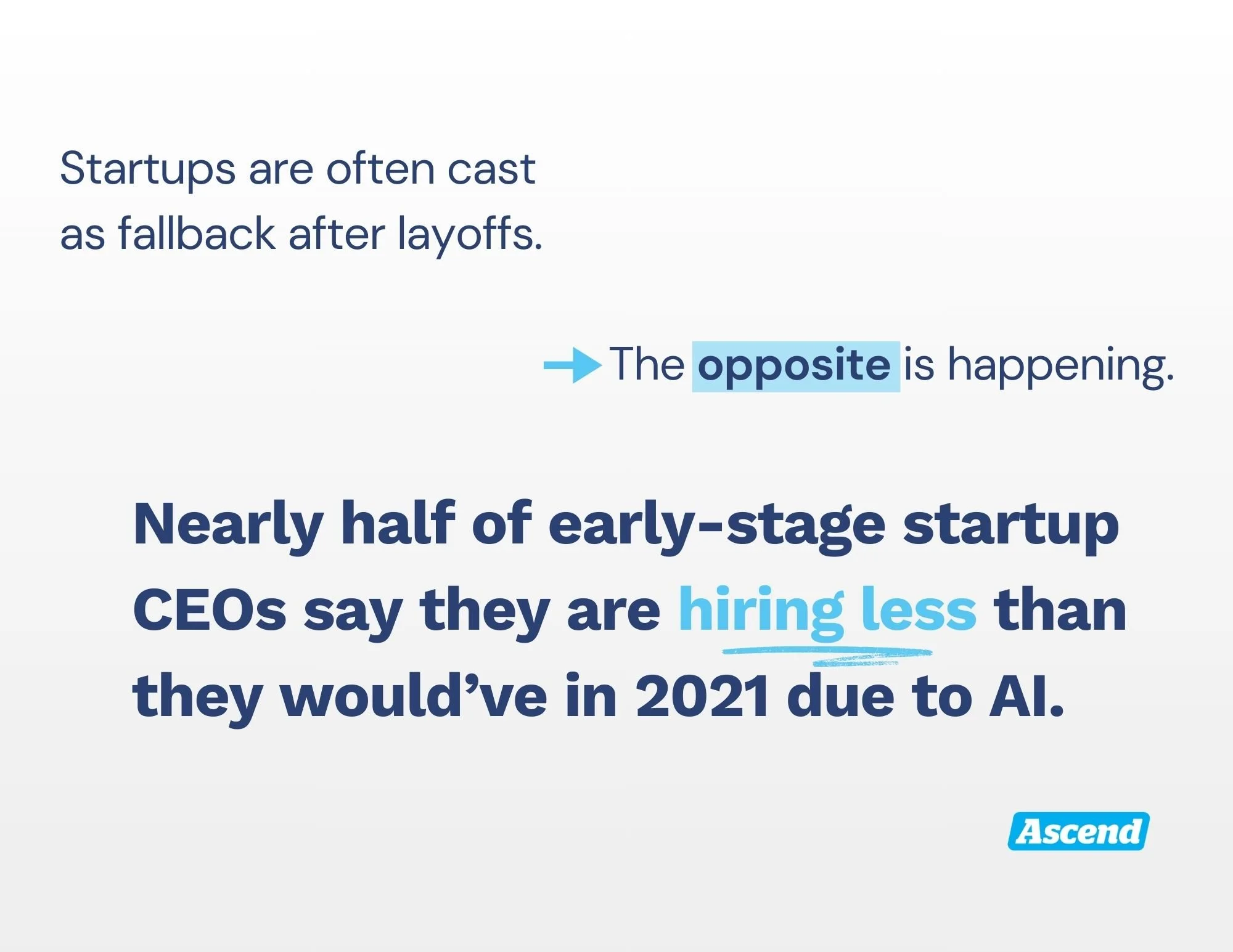

Conventional wisdom holds that startups function as a safety net in times of layoffs. As big companies shed workers, fast-growing newcomers are expected to absorb displaced talent.

It is a comforting narrative, and one that has resurfaced as Big Tech layoffs extended into early 2026, with more than 26,000 employees affected across 59 companies in January alone.

Data from an Ascend survey of early-stage startups tells a different story.

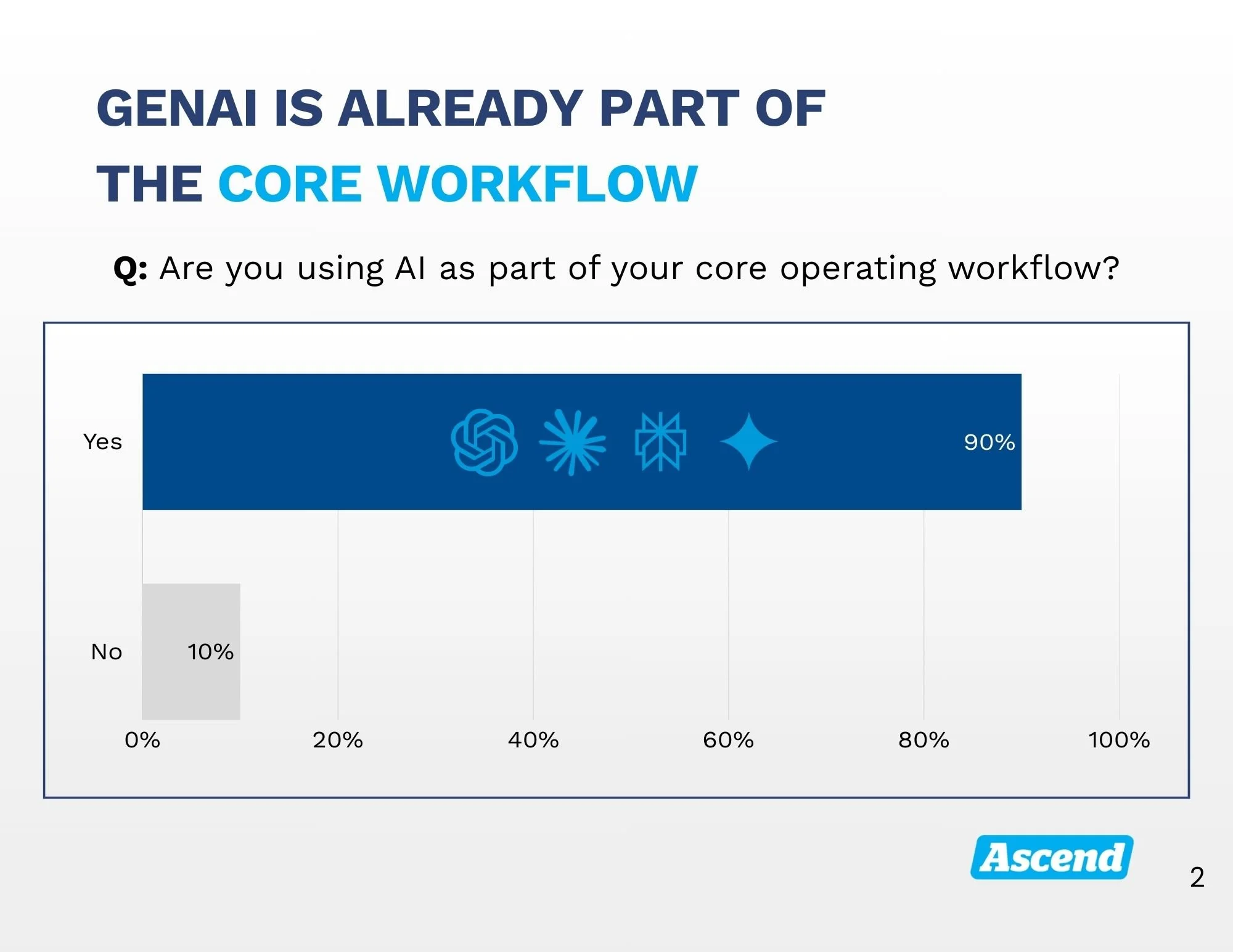

Among the VC-backed startups in our survey, nearly nine in 10 CEOs report actively using AI in the operation or building of their companies. Many say they are operating with significantly smaller teams than they would have needed just a few years ago.

Rather than acting as a counterweight to layoffs, startups appear to be following similar patterns as their larger peers, and in some cases doing so earlier and more decisively.

The difference lies in how those changes show up. At large companies, AI-driven efficiency tends to surface through visible layoffs. At startups, it shows up through hiring plans that never materialize and roles that are never filled.

To better understand how these decisions are being made, Ascend surveyed CEOs of VC-funded startups about how AI is used today, how central it is to their products and operations, and what it means for team size, hiring, and execution.

The goal was not to forecast long-term labor outcomes, but to capture how founders are designing organizations while they are still small enough for those choices to matter.

The survey reflects a narrow but intentional sample. Respondents were CEOs of VC-funded startups, primarily based on the West Coast, and overwhelmingly early stage.

The average company was founded in 2022. Most respondents were between pre-seed and seed. Excluding a small number of larger outliers, the median company had between one and 10 employees, with an estimated average team size of roughly 14.

These are companies still deciding which roles to hire in the first place.

Here are some key takeaways:

Eighty-nine percent of respondents reported using AI in the operation or building of their startup, while only 11% reported no usage. Adoption spans both AI-native and non-AI-native companies.

Roughly 30% said AI is the core product, another 27% described it as a major feature, and the largest share, about 41%, said AI is used internally but is not customer-facing. Very few characterized their use as experimental.

Most startups use multiple models. OpenAI and Anthropic were the most commonly cited, each used by more than 80% of respondents. Google’s Gemini followed at roughly two-thirds adoption. Open-source and alternative models appeared at lower but meaningful levels, reflecting a willingness to mix and match tools in pursuit of speed and cost efficiency.

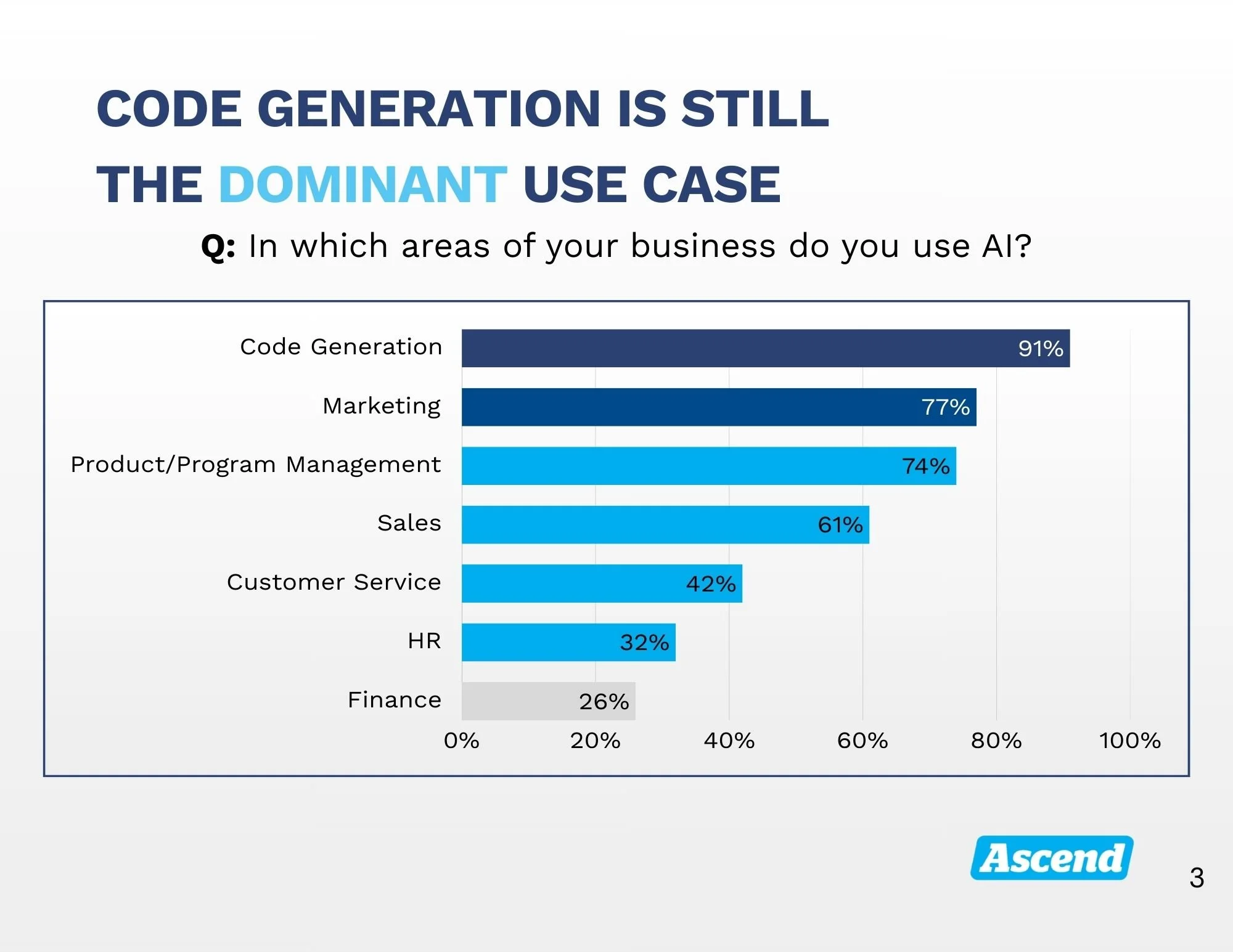

Where AI shows up most clearly is in work that directly affects execution velocity as code generation is nearly universal. Product and program management, marketing, and sales follow closely, with customer service also ranking high.

(Usage in HR and finance is present but less common, indicating that AI adoption tends to concentrate first in functions tied to building, shipping, and selling before expanding into back-office operations.)

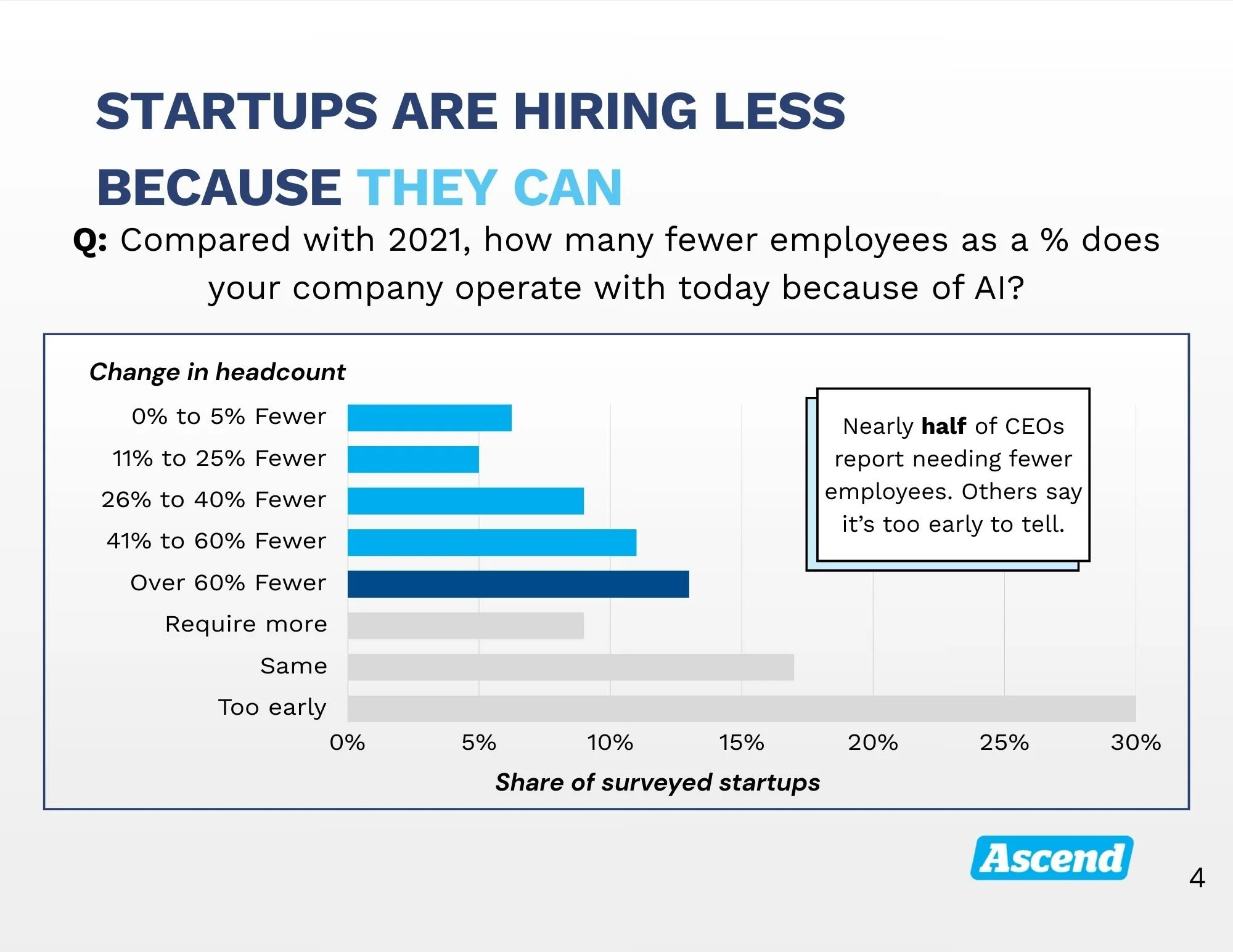

When founders were asked to compare their current team size with what they would have needed in 2021, responses varied. About 17% said they operate at roughly the same size, while 9% said they need more employees than they would have before 2022. Nearly 30% said it is too early to estimate. Among the remaining respondents, however, a clear pattern emerged. Many reported operating with fewer employees because of generative AI and automation, with several citing reductions in the 25% to 60% range and a smaller group reporting reductions of more than 60%.

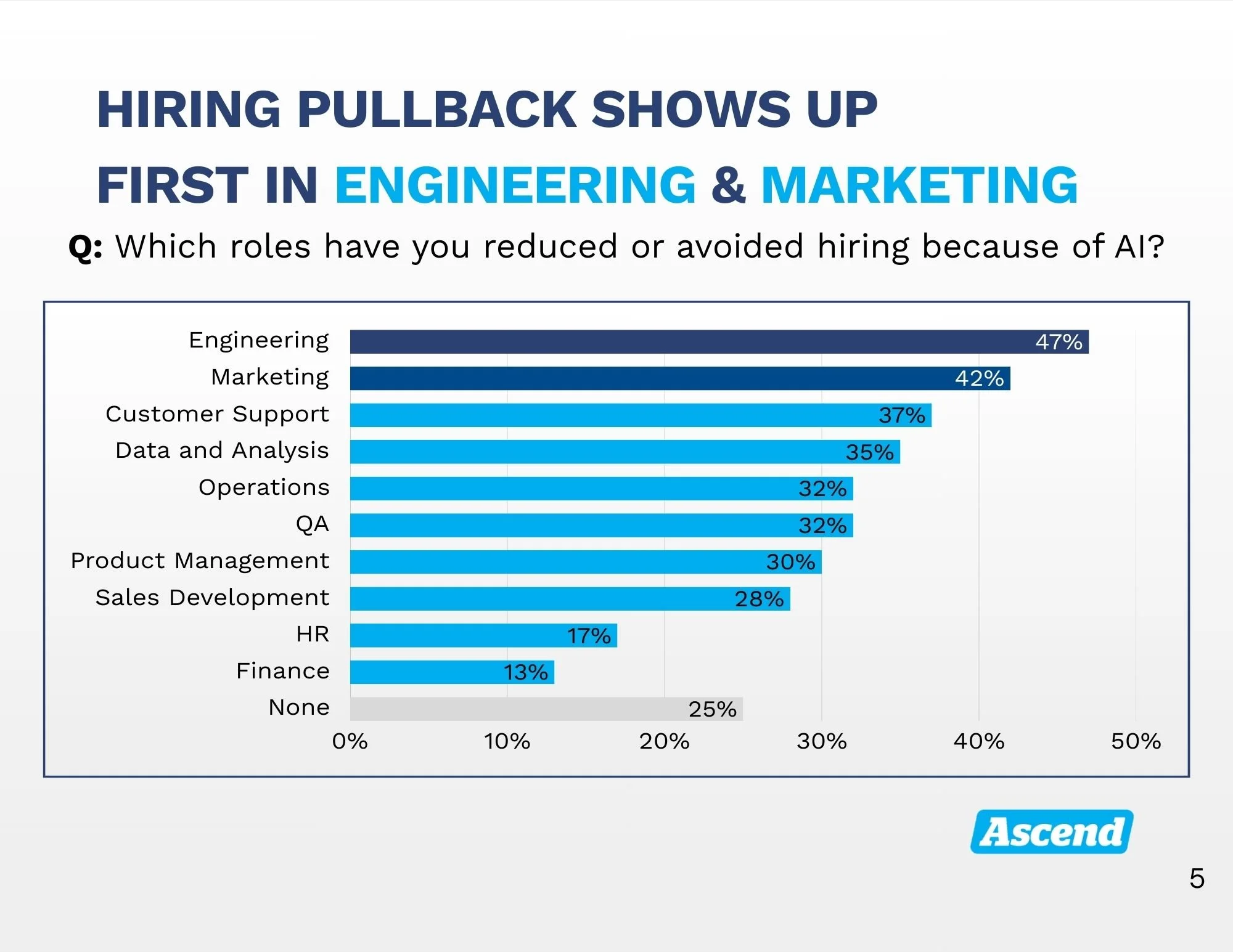

Those changes are not evenly distributed across roles. Engineering and marketing were most frequently cited as functions where hiring had been reduced or avoided, followed by customer support, operations, and data and analysis. Product management and QA also appeared frequently, while finance and HR were less commonly affected. Some companies reported no role reductions at all, underscoring that these decisions remain highly context-dependent.

Startups are reorganizing work in ways that mirror their Big Tech peers, and in some cases doing so at a faster pace. AI is reshaping how teams are built long before those effects show up in public headcount data, changing not who gets laid off, but who never gets hired in the first place.

At the earliest stages of company building, the impact of AI on work is subtle rather than dramatic. It accumulates one hiring decision at a time.

The limitations of the survey: sample size is modest at 70, respondents skew West Coast, and the companies are young enough that long-term impacts remain uncertain. The data is self-reported.